How to Lose $4.25 Billion in Five Weeks: The Still Unfolding Tale of New York's Hindenburg Research vs. PACS Group, One of Utah's Hottest Firms in 2024

On 04 November 2024, Hindenburg Research released a 15,000-word, deep-dive report alleging multiple misdeeds leading up to the April 2024 Initial Public Offering of PACS Group (NYSE:PACS), the Farmington, Utah-based owner, manager and operator of over 310 skilled nursing facilities in 17 states across the United States.

Since Hindenburg's report was published, PACS

— Announced on 06 November 2024 that it would not file in a timely manner (aka, on/before 15 November 2024) its quarterly report for its third quarter (ended 30 September 2024) due to what it "believes" are misleading third-party allegations, allegations that are being investigated by the "... company’s Audit Committee, with assistance from external counsel ...";

— Announced that it had received a Filing Delinquency Notice from the New York Stock Exchange on 20 November 2024 notifying the firm it has six months to come back into compliance by filing its Form 10-Q for its third quarter of 2024 or risk being delisted by the Exchange; and

— In the five-week period since Hindenburg disclosed its allegations against the Farmington-based firm, PACS Group has seen its market valuation slashed by over 63%, dropping to ~$2.4 billion last Friday (06 November 2024) down from a market capitalization of over $6.66 billion as of market close on Friday, 01 November 2024, the last trading day before Hindenburg published its report on Monday, 04 November 2024.

{Note: Hindenburg did disclose in its report that it had taken a "short" position in shares of PACS, essentially betting that the market cap of PACS would drop following publication of its report.}

Prior to 11 April 2024, I suspect that fewer than 1/10th of 1% of Utah's adults had ever heard of Farmington, Utah-based PACS Group before.

That's because even though PACS had grown to become one of the largest owner/operators and managers of long-term care / skilled nursing facilities (SNFs) in the U.S. since "... late 2012 when its predecessor was launched in California by co-founders Jason Murray and Mark Hancock," the firm actually had zero footprint in Utah except for its corporate headquarters and its Farmington-based staff.

But, as I noted in my Utah Money Watch writeup titled "Farmington-based PACS is Poised to Shock Utah's Biz Community with its $3.1 Billion IPO Slated to Hit Today, Thursday, 11 April 2024," PACS was set for what I anticipated would be an amazing year for the firm.

And clearly, the company has not disappointed.

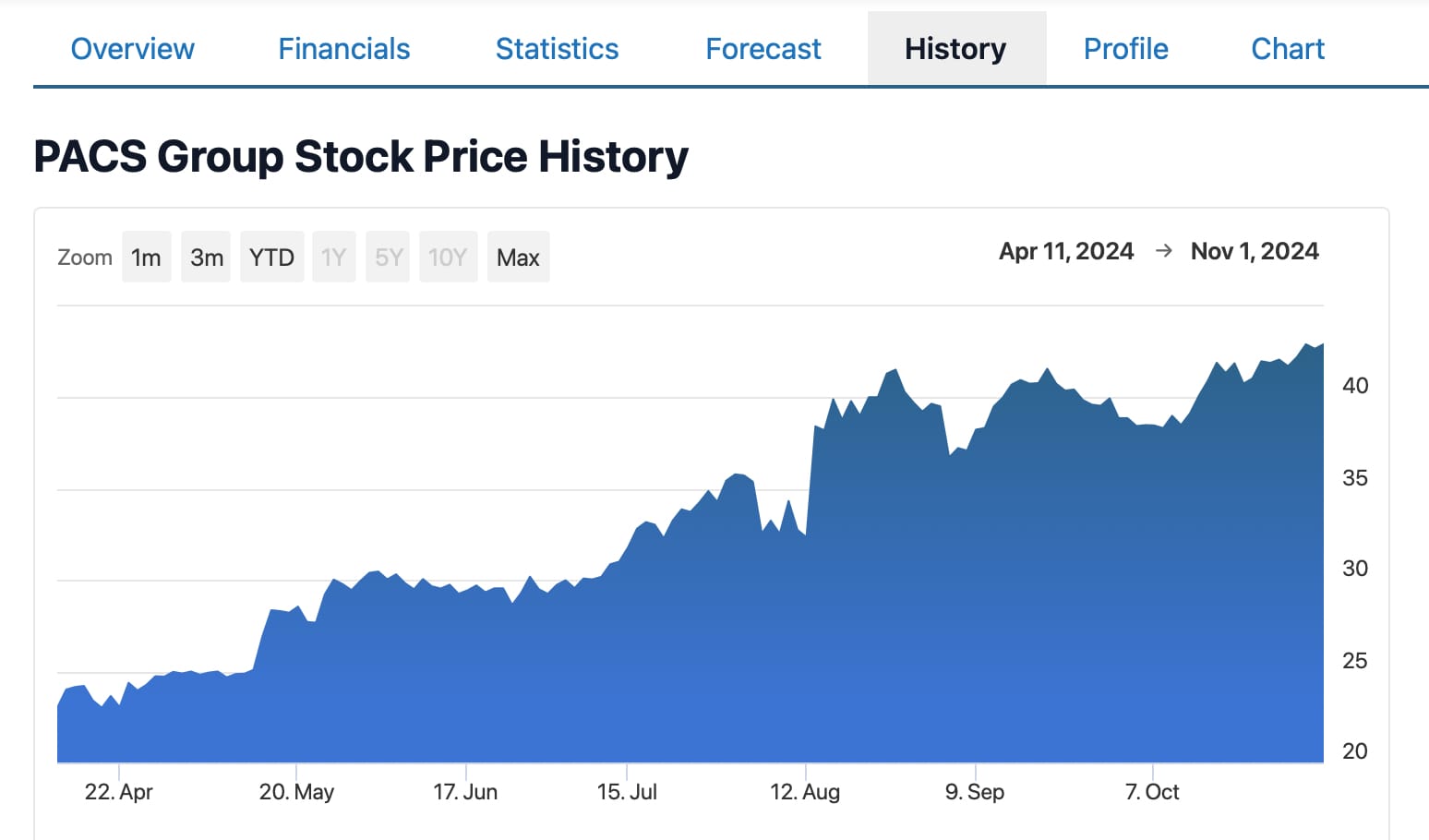

In fact, when you look at a stock chart for the PACS share price from its Initial Public Offering on 11 April 2024 through 01 November 2024, you can see what every investor hopes for in an investment, as it's mostly ...

Up and to the right.

As noted in that 11 April 2024 Utah Money Watch report, PACS had disclosed in its Prospectus filing on Form S-1/3 with the U.S. Securities and Exchange Commission that it had generated $3.1 billion in revenue in 2023 (ended December 31).

At the time, PACS "... own(ed) and/or provide(ed) services via 208 SNFs in nine states, namely

- "California (131 facilities with 14,610 beds/units),

- "South Carolina (24 facilities with 2,719 beds/units),

- "Colorado (20 facilities with 2,719 beds/units),

- "Arizona (9 facilities with 1,219 beds/units),

- "Kentucky (7 facilities with 936 beds/units),

- "Ohio (6 facilities with 637 beds/units),

- "Texas (5 facilities with 572 beds/units),

- "Nevada (4 facilities with 335 beds/units), and

- "Missouri (2 facilities with 160 beds/units)."

And for its work, PACS generated net income of nearly $113 million in 2023.

As reported by Utah Money Watch five days later, with the overallotment of shares provided to its underwriters through the IPO process, PACS sold "... slightly over 21.4 million shares of PACS common stock ..." at $21.00 per share, producing "... over $450 million in gross proceeds from the offering" for PACS.

From mid-April through late fall, things went quite well for PACS, with a few of its highlights including that it

- Reported record quarterly revenue on 13 May 2024 of $934.7 million for its first quarter (ended March 31), a 31.4% increase over the comparable period in 2023;

- Purchased the operations of 53 SNFs in the western U.S. for $0 in acquisition costs while concurrently investing $15 million in a real estate joint venture, adding over 2,500 additional skilled nursing beds and more than 1,330 additional assisted living and independent living units to its portfolio;

- Held a secondary offering in the first half of September, raising $101 million in gross proceeds for the firm, while selling shareholders received $589 million in proceeds from the sale of ~16.26 million of their common shares of PACS stock; and (as noted above)

- By 01 November 2024, the stock price of PACS common shares reach a closing price of $42.94, a jump of nearly 205% from the IPO offering price of $21.00/share — a jump that pegged the market capitalization of PACS that day at $6.66 billion.

Not bad for a six-and-a-half-month run.

Not bad at all.

And then Hindenberg happened.

Hindenburg Research: The Anti-Stock Promoter

For readers not familiar with Hindenburg Research, the company "... specializes in forensic financial research."

More specifically, the Hindenburg website says:

"Our aim is to provide critical insights and evidence to the public, market and regulators to effect meaningful change. To date, Hindenburg and its founders’ investigations have preceded SEC fraud charges against 65 individuals, Department of Justice criminal indictments against 16 individuals, and foreign regulator sanctions and fraud charges against 6 individuals."

Additionally, the website explains that it "... look(s) for situations where companies may have any combination of:

- "Accounting irregularities,

- "Bad actors in management or key service provider roles,

- "Undisclosed related-party transactions,

- "Illegal/unethical business or financial reporting practices, (and)

- "Undisclosed regulatory, product, or financial issues."

So, when Hindenburg published the following report at 6am (ET) on Monday, 01 November 2024 — "PACS Group: How To Become A Billionaire In The Skilled Nursing Industry By Systematically Scamming Taxpayers" — a titillating headline, to be sure — I consciously chose to sit back and wait to see what, if anything, would happen in the ensuing days and weeks.

So I did.

And now, five-plus weeks later, a stock performance chart from 01 November 2024 through market close this past Friday (06 December 2024), shows clearly that the investment world has not been kind to PACS Group and its shareholders.

In fact, the share price downdraft has been brutal.

According to online reports, PACS currently has 155.18 million shares outstanding.

Hence, based upon its closing price of $42.94/share on Friday, 01 November 2024, PACS had a market capitalization/valuation that afternoon/evening of slightly over $6.66 billion.

By last Friday (06 November 2024), however, just under five weeks after Hindenburg dropped its bombshell report, the PACS share price had been slashed to $15.51/share, giving the firm a market cap of $2.4 billion.

Yes, that's a valuation loss of over $4.25 billion.

In. Five. Weeks.

Percentage-wise, that's a market cap drop of over 63%.

So What Happened?

First off, if you (as a reader) are not clear about this, any time Hindenburg chooses to publish a research report about a firm, its executives, and/or its practices, that's not a good sign.

Does it mean that Hindenburg or its principal(s) are without fault?

No.

Or, because Hindenburg often takes a "short position" in the securities of a company it reports about, is it possible to make a case that doing so is unethical or manipulative?

Perhaps.

But after reading several of its reports now, including the most recent one about PACS Group, I'll just say that the info shared in Hindenburg's reports can be both convincing and quite compelling.

At a minimum, such reports from Hindenburg can also serve as a shocking smack-upside-the-head for both firms and investors alike.

This being the case, I will only briefly summarize the Hindenburg allegations against PACS Group by quoting these four paragraphs from the very beginning of Part 1 within the 15,000-word report:

"Our 5-month investigation into PACS included an in-depth analysis of corporate financials and more than 900+ publicly available facility-level financial reports, as well as interviews with 18 former PACS employees and an industry expert.

"Far from finding evidence of a sophisticated “turnaround” strategy, we uncovered a series of fraudulent schemes and aggressive practices seemingly designed to siphon as much money as possible from taxpayer-funded government healthcare programs into the pockets of PACS co-founders Mark Hancock and Jason Murray.

"Evidence shows the most aggressive of these practices was a management-driven, company-wide scheme to defraud Medicare through the COVID emergency, evidenced by anomalies in PACS’ Medicare revenue, and corroborated by more than a dozen former PACS employees, ranging from frontline clinical staff to regional managers.

"We believe this scheme funded PACS’ aggressive acquisition strategy throughout COVID and drove substantially all of its earnings from early 2020 to the end of 2023, giving investors the illusion of legitimate growth and profitability leading into its IPO."

Clearly, these are very serious allegations against PACS, its executives, management, and practices.

So rather than go into greater detail about the specifics of what Hindenburg alleges against PACS, readers interested in reading/reviewing the full report can do so here.

However, with the publication of the Hindenburg report, here's what's happened since then:

- By market close on Monday, 04 November (the day the report was published), the PACS share price had dropped $11.93 to close at $31.01.

- On Tuesday, the share price dropped again, but only by $1.47/share to close at $29.54.

- But then on Wednesday, 06 November 2024, PACS announced in a news release that it would be unable to file, in a timely manner (aka, on/before 15 November 2024), its quarterly report for its third quarter (ended 30 September 2024) due to what it "believes" are misleading third-party allegations, allegations that are being investigated by the "... company’s Audit Committee, with assistance from external counsel ...." That day, the price of PACS common shares dropped to $18.09, a loss of $11.45 in one day of trading.

- Two weeks later (on 20 November 2024), PACS received a Filing Delinquency Notification from the New York Stock Exchange that the company had not met its obligation to file its quarterly report on Form 10-Q for the third quarter ended September 30. In its Form 8-K filing about this Notice, PACS noted that it intended to meet the requirement within the six-month period granted to it by the NYSE.

- Since then, the price of PACS shares have closed as low as $14.62/share (on Thursday, 05 December 2024) before closing up at $15.51 this past Friday, November 6th.

Additionally, it should be noted that PACS announced on December 5th that it had closed an acquisition on the "... operations of 11 skilled nursing facilities in Tennessee on December 1, 2024," adding 1,310 skilled nursing beds in the process.

However, financial terms of this transaction were not disclosed.

Additionally, PACS explained in the same news release that since 31 October 2024, the company has "... acquired a total of 38 facilities ... adding 4,700 skilled nursing beds to its portfolio."

So ... What's Next?

In all honesty, the claims made by Hindenburg against PACS Group, its founders, executives, management, and practices are quite serious.

And to their credit, it's clear to me that the PACS executive team and Board are approaching these claims as such (at least from what little has been disclosed by the company).

On a tangential yet related point, I think it should be noted that of the seven investment banking firms that have analysts that provide research analysis on PACS, all of them have only published reports that provide positive ratings on the company, stock recommendations of

- Buy,

- Outperform, or

- Overweight,

for a total of 19 separate reports (as reported by Yahoo! Finance).

Of these 19 reports, only Stephens & Co. has published an updated report since 04 November 2024, a report that maintained its Overweight recommendations for PACS, with a recalibrated share price target of $31/share down from $48/share.

That said, the Stephens report "... maintain(ed) its 2024-2026 adjusted EBITDA estimates" for PACS.

This being the case, I am curious to see how/when the analysts at the other six investment banks —

- Citigroup,

- Macquarie,

- Oppenheimer,

- RBC Capital,

- Truist Securities, and

- UBS —

update their recommendations regarding PACS Group, if at all.

Regardless, given what is potentially at stake, I would be shocked to see PACS make any financially or legally material announcements until the firm's Audit Committee and external counsel have had a chance to review, and address, each allegation made by Hindenburg in its report.

If I'm correct, that would mean no quarterly report filings from PACS before the audit/legal counsel review is completed.

That might also mean a delay in the filing of the company's 2024 Form 10-K Annual Report filing with the SEC for the year ended December 31.

Additionally, perish the thought, but if the Audit Committee / legal counsel find material credence to any of Hindenburg's claims, the outcome could be as great as a need to restate financial figures for one or more of the audited periods included in the PACS Group Form S-1/3 Prospectus.

And if that were to occur, things could get messy/ugly quickly.

So ... like you ... I will wait and see how everything progresses from here.

But for now, PACS and its shareholders are sitting on the five-week evaporation of over $4.25 billion in market value in just five weeks time.

Ouch!

Publisher's Note

Are you tired of NOT having access to timely Utah-focused monetary, financial, and/or business news, context, and analysis?

That's easy to fix — just become a subscriber of Utah Money Watch. Today!

Simply,

1. Click on a "Subscribe" button on any Utah Money Watch webpage,

2. Enter in your name in the proper field in the popup window that appears on-screen, and

3. Enter your preferred email address in the proper field too.

"Yes," it really is that simple.

And it IS free ... for now, at least.

So, thanks.

I hope to see you as a Utah Money Watch subscriber today.

David ("Poppa P") Politis,

Publisher, Editor & Founder

Utah Money Watch

P.S. For context, the purpose of Utah Money Watch is to publish news, information, context, and analysis NOT available through any other source.

[You might think of us as the inverse of Bloomberg, CNBC, and/or The Wall Street Journal. In other words, we are passionately focused on uncovering the most important monetary, financial, and/or business news and information that impact the organizations and people of Utah first, followed by regional news/info second, and national/international info/news last of all.]

To that end, this article/report was originally published and distributed to our Subscribers at approximately 7:05am (MT) on Monday, 09 December 2024.

However, if this report/article came to your attention sometime after this date/time and you'd like to change that, then (to become a subscriber), please follow the steps above.

Thx. DLP

Comments ()